Buy-to-let has had quite the journey. Mortgages for buy-to-let properties were first introduced to the UK in the mid-1990s and proved to be an attractive proposition for investors from the outset. For years, the private rented sector was a growth story.

But in more recent times, the sector has weathered a storm of tax changes, interest rate hikes, and regulatory reform. Add in upcoming legislation, like the Renters’ Rights Act and new energy standards, and it’s clear the landscape has shifted.

Yet landlords haven’t packed up and left. In fact, some are doubling down.

According to UK Finance, over 58,000 new buy-to-let mortgages were approved in Q1 2025 – up nearly 40% on last year. Loans for new purchases jumped 61%, albeit from a low base. While buy-to-let still makes up around 10% of total transactions, demand hasn’t disappeared entirely.

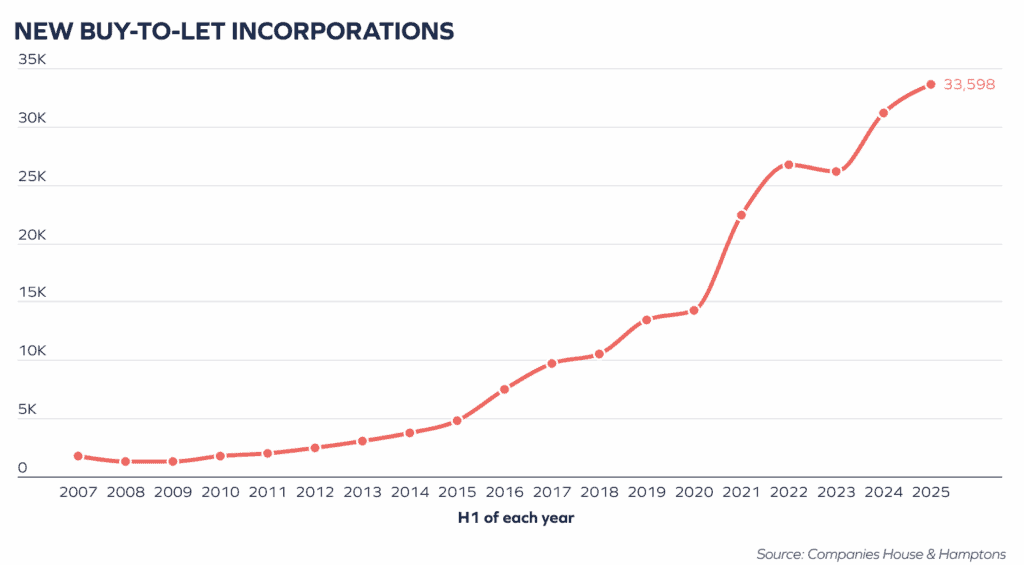

And landlords aren’t just buying – they’re incorporating. A record 33,598 buy-to-let companies were set up in the first half of 2025. Even after April’s stamp duty increase, incorporations rose sharply in May and June.

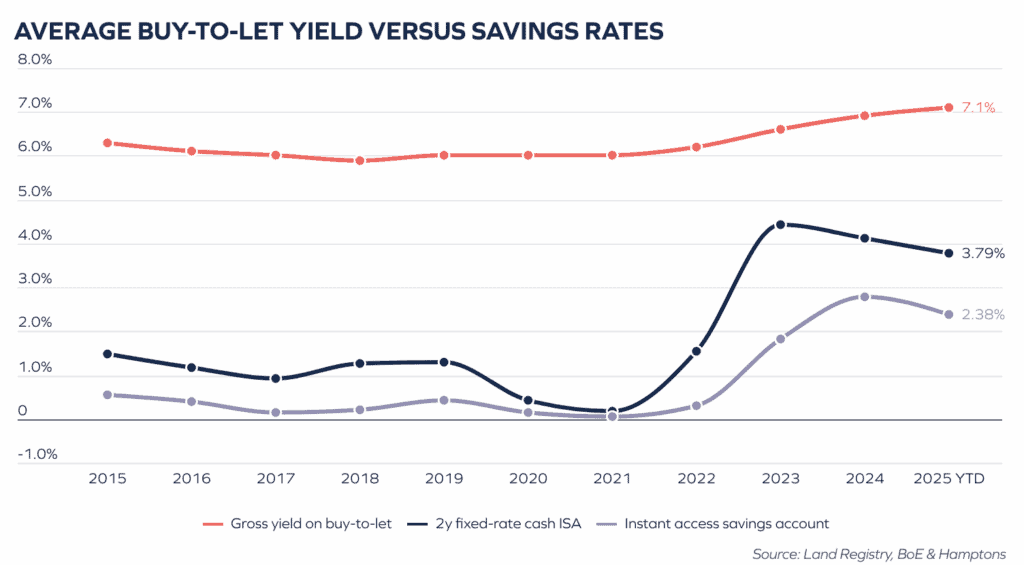

Returns are improving too. Gross yields on new purchases now average 7.1% across England and Wales, with one in four landlords achieving double-digit returns. The North East leads the pack at 9.3%, while London has climbed from 4.1% in 2020 to 5.7% today. These stronger yields are helping landlords absorb higher costs, from mortgages to maintenance.

The investor profile is changing. Since 2016, the share of newly incorporated buy-to-let companies with at least one non-UK shareholder has grown from 13% to 20%. Indian and Nigerian investors are leading the charge. While London remains a hotspot, overseas ownership is rising fast in the Midlands and Scotland.

So what’s keeping investors engaged? For many, it’s the appeal of bricks and mortar. With savings rates dipping and stock markets wobbling, property is often seen to offer stability and income. And with house prices now rising faster than rents, some see this as a window to lock in strong yields.

Falling mortgage rates have also helped. In a sector where leverage matters, even small rate cuts can make a big difference. That’s been a key driver of recent activity.

And let’s not forget the fundamentals. The UK has a chronic shortage of rental homes, and younger generations are renting for longer. They’re less likely to become landlords themselves, which means demand is rising while supply stays tight. We expect rents to grow by 3.5% in 2026 and 3.0% in 2027.

What we’re seeing is a shift. The sector is consolidating, with fewer landlords managing larger, more professional portfolios. It’s no longer the gold rush it once was, but for those willing to adapt, buy-to-let remains a solid long-term play.

Read more about our rental growth forecast here.