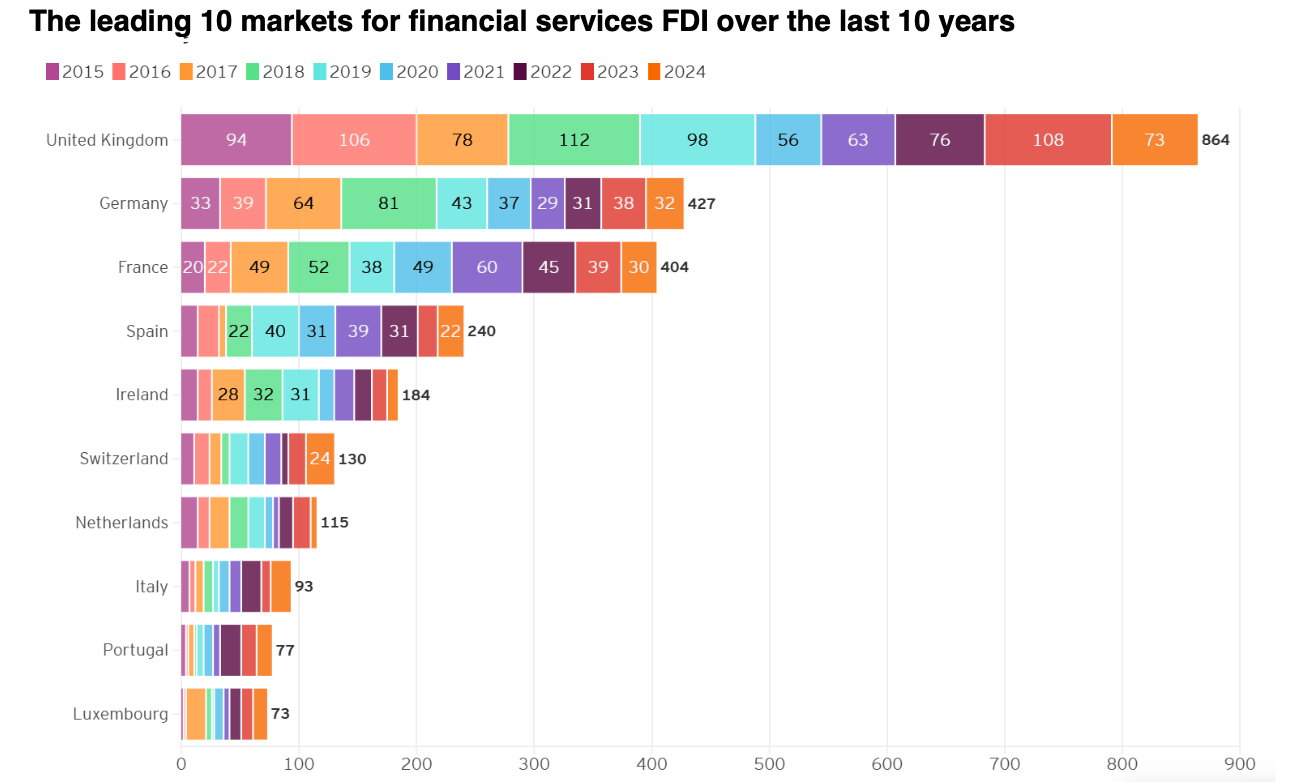

The UK continues to be Europe’s most attractive location for foreign direct investment (FDI) into financial services, recording 73 projects in 2024—despite this representing a 32% decline from 108 in 2023, according to a recent EY survey.

Germany ranked second with 32 financial services projects (a 16% annual decrease), followed by France with 30 (down 23%).

Across Europe, total financial services FDI projects fell by 11%, from 329 in 2023 to 293 in 2024. The UK accounted for a quarter of all such projects, although this was down from 33% the previous year. Germany secured 11% and France secured 10% of these projects – both unchanged from 2023.

Martina Keane, EY UK and Ireland Financial Services Managing Partner, said, “The UK has retained its position as Europe’s most attractive destination for financial services investment, despite investment falling across the region. The strength and depth of the UK’s financial services sector continues to capture global investor confidence – particularly as they navigate challenging market conditions. But competition is fierce, and while the UK industry is a clear leader, we cannot ignore the fact that investment levels have declined over the last year.

“Both industry and Government are taking positive action to prioritise growth and innovation in UK financial services, and this collaboration must continue. Future success rests on not just maintaining, but growing the attractiveness of the UK’s financial services sector on the global stage. To do this, we must build on our inherent strengths and prioritise progressive regulation, innovation and the continued establishment of key international trade relationships.”

While total project numbers declined, the number of ‘new’ financial services projects across Europe rose slightly—from 233 in 2023 to 234 in 2024. Of the UK’s 73 projects, 53 were new, down from 85 the previous year.

New project figures also fell in Germany (from 32 to 28) and France (from 22 to 17), while Spain saw an increase from 14 to 21, and Switzerland rose from 11 to 21.

New project figures also fell in Germany (from 32 to 28) and France (from 22 to 17), while Spain saw an increase from 14 to 21, and Switzerland rose from 11 to 21.

Employment from financial services projects across Europe declined following three years of growth. In the UK, disclosed job numbers fell by 52%, from 5,019 in 2023 to 2,408 in 2024. Across the EU, employment was down 33% year-on-year.

London remained the leading European city for attracting financial services FDI, though project numbers fell from 81 in 2023 to 39 in 2024. Paris came second with 23 projects (down from 31), while Madrid and Zurich tied for third, each securing 14 projects—up from 11 and 9, respectively.

London also topped the list for new projects, with 34 in 2024, though this was down from 69 in 2023.

The US was once again the largest source of financial services investment into Europe, backing a quarter of all projects in 2024 despite a 21% decline from 91 in 2023 to 72.

The UK remained the primary recipient of US investment. Although the number of US-backed UK projects fell by 26% (from 38 to 28), the UK attracted a higher share of US investment (38%) than its 10-year average (34%).

Despite most major markets experiencing a decline, several countries bucked the trend and saw year-on-year increases in investment. Switzerland, now ranked fourth in Europe for financial services FDI, recorded a 60% increase (24 projects, up from 15). Spain (fifth) saw a 29% rise (22, up from 17), Italy (sixth) more than doubled its total (17, up from 8), and Luxembourg (seventh) saw a 20% increase (12, up from 10).

Omar Ali, EY Global Financial Services Leader, said, “Whilst geopolitical and macroeconomic uncertainty has weighed on investor sentiment and business confidence this past year, cross-border investment remains key for global financial services firms as they look for growth and competitive advantage. Global investors are undoubtedly still committed to Europe’s deep capital markets and highly skilled workforce and although investment fell both overall and in the region’s biggest markets in 2024, a number of financial centres bucked this trend. Switzerland, Spain, Italy and Luxembourg all recorded a rise in foreign investment, in part due to the progressive policy environment and specialist sector expertise they offer.

“Outside of Europe’s borders – notably in New York, Singapore and Hong Kong – competition is strong. With FDI levels down on previous years, it is more important than ever that Europe’s major markets find ways to outwardly demonstrate the pull factors that investors are looking for and collaborate where needed to keep investment within the region.”

According to a global financial services investor sentiment survey in May 2025, 86% of investors believe the UK will retain or improve its level of financial services attractiveness over the next three years (up from 75% in 2024).

London is considered the most attractive European city for financial services foreign investment over the next year (54%), ahead of Frankfurt (45%), Paris (40%) and Dublin (37%).

At a country level, Germany was viewed as the most attractive European country for financial services investment (47%), followed by the UK (45%), France (38%), and Switzerland (24%).

London’s biggest rivals for financial services foreign investment over the next three years were named as New York (59%), Frankfurt (43%), Paris (41%), Singapore (39%) and Hong Kong (39%).

Following US tariff announcements in March, investor sentiment favours the UK over the EU and US for FDI. Investors surveyed were more likely to invest in the UK (44%) than in the EU (39%) or the US (32%).

However, UK tariff announcements have increased caution in some investors. When asked if they were now less likely to invest in these markets, investors cited the US (61%), the EU (55%) and the UK (52%) as areas of increased hesitation.

Key strategic investment areas cited by investors included support for small and medium-sized businesses, tech and innovation, R&D funding and access to business capital.