The FTSE 100 index is up just shy of 12 per cent over the past year, and ahead of the US and European indices this year to date.

Tom Moore, who runs the Aberdeen Equity Income Investment Trust, confesses to being a little surprised at how well the market is doing.

He says: “The economic data wouldn’t point to it. And when we speak with company management in the UK, they are very pessimistic; they were more optimistic in 2019, even with all of the Brexit stuff happening, than they are now.”

But he adds that while the economy does not justify the improved outlook, his view is that structural factors may mean inflows have come into the asset class for the first time, even if it is only because institutional investors have stopped selling.

Moore says: “The data shows that in 1995 [so 30 years ago] UK pension funds and insurance companies owned about 50 per cent of the UK equity market, the figure is now about 5 per cent, but arguably it won’t get much lower, and even a small uptick in the level of buying of UK equities by international investors could be making a big difference.”

But is the improved performance of the asset class driving a greater level of interest from advisers?

Benji Dawes, a UK equity fund manager at Premier Miton, says he has spent the summer doing “breakfasts, lunches and dinners” meeting advisers to promote his funds, and says “there has been a lot more interest in terms of the number of people attending and their level of engagement — we haven’t seen it like this for five or six years.”

Imran Sattar, UK fund manager at Liontrust, says international buyers coming back to UK equities have driven returns.

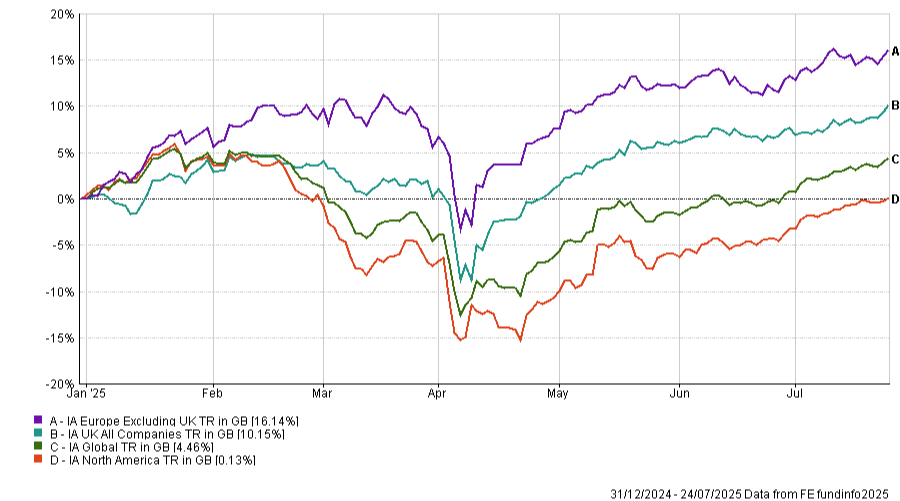

Data from the Investment Association, as illustrated in the chart below, shows the extent to which investors have been withdrawing capital from UK equity funds, and the slightly improved recent picture.

But is the current strong performance of the UK market a mere function of the market cycle moving the FTSE’s way for the first time in years, or is something more structural going on?

David Smith, who runs the Henderson High Income trust, says something structural may be happening.

He says: “The years after the global financial crisis were a period of very low interest rates, that created the conditions for growth stocks to outperform, and there are more of those in the US, whereas the UK market is full of value stocks, which don’t do as well when interest rates are low. But we are probably at a stage where rates are not going back to the previous very low levels, which could mean the recent trend of UK outperformance persists.”

It is a trend that is not unique to the UK market, according to Barry Galvin, head of equities at Amundi, who says the same trend is evident in Eurozone equity markets, as investors have prioritised diversification away from the US.

But he says the outperformance of US equities has not been based solely on exogenous factors such as interest rates, as, in his view, US companies have also deserved to trade at a higher multiple due to superior earnings growth, in part boosted by fiscal policies which continue under Trump, and says: “The attractions of the US market haven’t gone away. It has delivered standout earnings growth for many years.”

Caroline Shaw, multi-asset investor at Fidelity, says: “We are not negative on the UK at all, but nor are we banging the drum for them. The return on equity being delivered is OK, it’s fine, but it is not as good as the returns from the US.

“We are slightly overweight to the asset class relative to our peer group, but with the labour market deteriorating and other factors, we think there could be certain sectors of the UK market that are hit very hard, and others which could do well, and with that in mind, most of our UK allocation is to active managers, rather than the index.”

Ken Wotton, a UK equity fund manager at Gresham House, says that regardless of investors’ perspective on the outlook for the US market, “I think there has been a realisation in recent months that diversification is sensible, and that has boosted demand for equities outside of the US”.

He says there has been a pick-up in interest from investors wanting to discuss UK equities, which he expects will eventually translate into better inflows.

Sterling effort

A curiosity of the FTSE 100 has long been that it tends to perform best when the currency is weak, and the currency is often at its weakest when the economic outlook is most negative.

An example of this is performance of the index in late 2016, as the market rose in the immediate aftermath of the Brexit referendum vote, as sterling fell.

The weaker pound boosts the returns of companies in sectors such as oil and mining, as those products are sold in dollars, with the revenue then translated back into sterling, so the more pound a dollar buys, the higher the income.

But the FTSE 100’s rise in 2025 has coincided with sterling appreciating by around 9 per cent against the dollar.

Kunal Kothari, UK equity fund manager at Aviva Investors, says that while it is unusual for sterling and the FTSE to perform relatively well at the same time, many of the sectors that have driven the growth of the FTSE, such as defence, which is 6 per cent of the index, are “currency agnostic”.

He notes that while predicting currency movements is hard, a scenario where the dollar strengthened against sterling could lead to the strong performance of sectors such as mining and oil, which could provide another opportunity for the FTSE to rise.

Shaniel Ramjee, co-head of multi-asset at Pictet Asset Management, is one investor who has not been rushing to increase his UK holdings. He says he regards the European peers of some of the largest UK companies as being better investments, and trading at cheaper valuations.

Whether it is the start of a sustained re-rating for UK equities, or just a favourable point in the cycle, it will impact client portfolios in the coming years.

David Thorpe is senior investment editor at FT Adviser