“If you take the costs out of real estate transactions, the returns [for apartments] are sub 4 per cent a year as costs like maintenance, agent fees, rates, insurance, repairs, stamp duty, and strata are hidden, high, and constant.”

When Ferrando shared these views on the investor website Livewire in January under the title “Residential property is a sub-par way to grow your wealth”, he received a barrage of criticism.

That’s perhaps not surprising, given property speculation is practically a national sport: 2.2 million Australians owned an investment property in 2021 (the latest figures are available), which is the equivalent of about 20 per cent of taxpayers.

Let’s take a closer look at Ferrando’s hypothesis. He says typical buy-to-let investors in Brisbane, Sydney or Melbourne will pay a deposit of 35 per cent and borrow 65 per cent from a lender.

They then lease the property and gear it negatively, which means expenses incurred (including borrowing costs) are deducted from income.

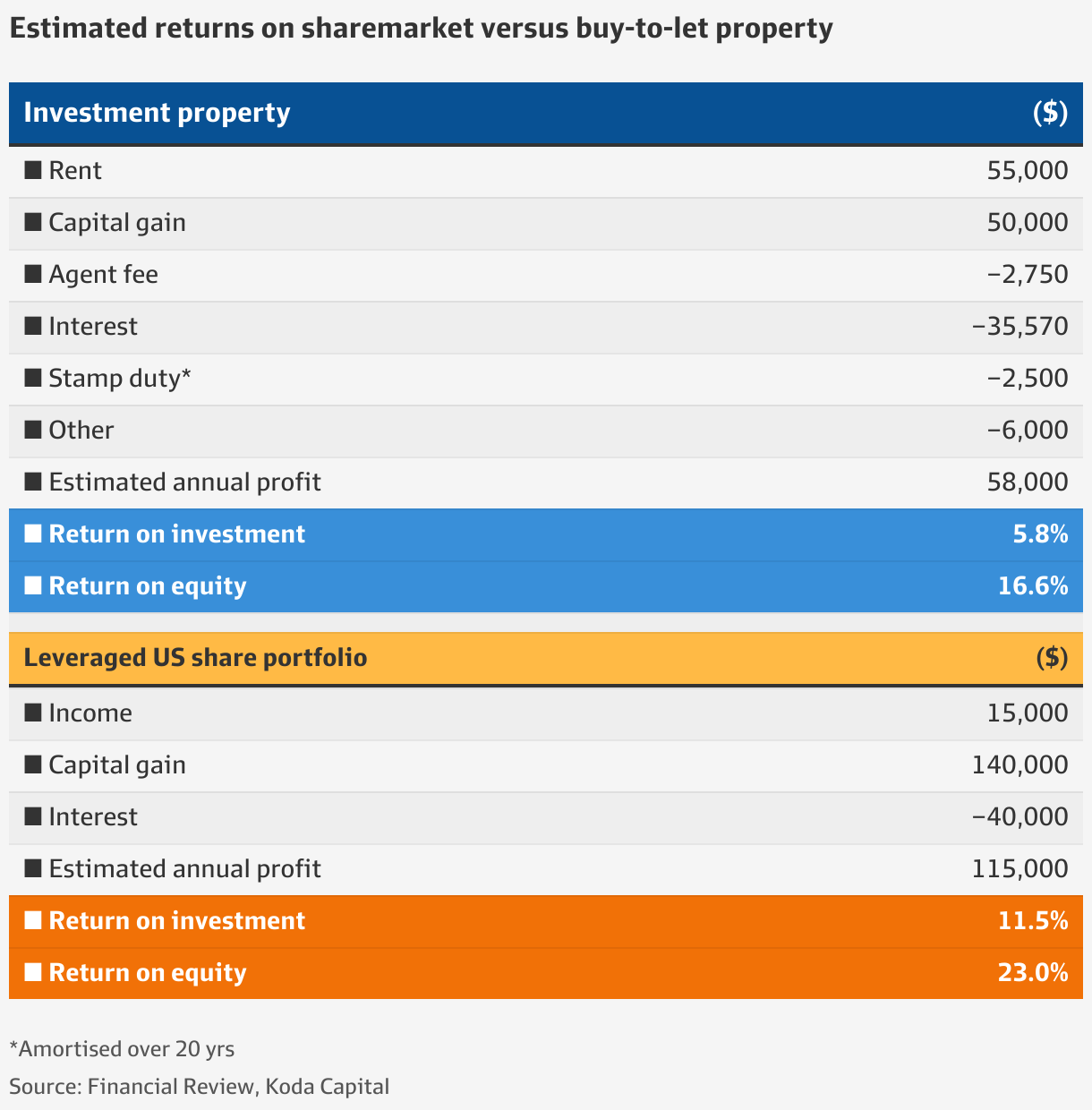

The basic investment thesis is that buy-to-let investors can profit from leverage as they can make returns in the form of rent and capital growth on a $1 million asset after spending $350,000.

But Ferrando says anyone with savings beyond those needed to own a primary place of residence could also obtain leverage – known as a margin facility – on a share portfolio with a broker.

“I say, buy real estate if you want to enjoy it every day, but don’t buy it with your investment dollars.”

The maths

Take a hypothetical $1 million share portfolio with $500,000 committed by the investor and $500,000 committed by a broker on margin (accruing interest to be repaid). It could return 11.5 per cent a year after the interest paid on the margin debt and assuming an average return of 14 per cent per year, split across the Nasdaq and S&P 500.

The return on equity – as a measure of profit on the investor’s capital of $500,000 – is 23 per cent, or $115,000 per year based on growth of $155,000 from dividend income and capital returns, minus costs of $40,000 on the margin debt.

By comparison, as the buy-to-let investor borrowed $650,000 to own the property, the return on equity – as a measure of profitability on the leverage – is an inferior 16.57 per cent, which is equal to a $58,000 profit from the $350,000 committed to buy the asset.

To compare the return on investment (ROI) on a $1 million investment property leveraged to 65 per cent, Ferrando deducts $47,000 per year in estimated costs to own the property from rental income ($55,000) and assumed capital growth of 5 per cent each year ($50,000), to equal a net return on investment of $58,000 per year or 5.08 per cent.

Meanwhile, the return on investment on a leveraged US share portfolio assuming a robust 14 per cent compound growth rate is almost double at 11.5 per cent per year, largely because the costs to run a share portfolio are far lower.

Ferrando says the US sharemarket’s superior returns of 14 per cent per year are realistic going forward, as the American government’s growing debt pile will finance spending programs that flow through to higher corporate profits, and therefore sharemarket returns.

“If you add the November 2023 and December 2023 [US government’s] monthly deficits $US317 billion and $US128 billion respectively, and annualise those two combined months, you end up with a deficit of $US2.67 trillion. Assuming US GDP is $US23.5 trillion, the current-run-rate deficit is 11.4 per cent,” he says.

In 2023, the US fiscal deficit equalled $US1.7 trillion or 6.3 per cent of GDP as the country enjoyed a jobless rate of about 3.6 per cent for much of the year in a combination that helped propel the Nasdaq and S&P 500 to record highs this year. Ferrando uses these figures to justify his 14 per cent return projection for the US sharemarket.

Australian residential property prices neared a record high in February despite 13 rate increases since May 2022, with houses gaining 84.7 per cent on average and units adding 40.7 per cent over the past 10 years.

Ferrando’s comments relate only to holding US shares. But for context, the S&P/ ASX 200 jumped 34 per cent from 5092 points to 7742 over the same period, although these examples exclude the significant impact of dividends or rental income for both asset classes.

Leverage and location

Michael O’Hara, a Perth-based adviser at Wealth & Security Planners, says it’s important to remember that leverage is easier to obtain on property than shares. Moreover, property as an asset class is less likely to crash than shares, which bombed during the global financial of 2009 and the pandemic slump of 2020.

“The studies I’ve seen over 37 years show residential property earns at a similar rate to Australian shares,” O’Hara says.

“The mix of income and capital growth is different, but the total return is similar. What makes property stand out from shares is the ability to leverage exposure and in a way that’s cosseted by preferential lending and government policy.

“Leverage takes advantage of a banking system built on residential real estate. It’s a system that assumes real estate is inherently ‘safe’. And in many ways, it is.”

Banks allow incredible leverage that is lower-risk and not available anywhere else, O’Hara says.

“If a 95 per cent loan-to-value property goes into negative equity, banks will stop doing valuation checks. They’ll balance that location on their books with others that show more promise.”

But if leverage in shares was available at the same rates and under the same terms as property, shares would win, says O’Hara.

“And many people are not suited to being landlords,” he says. “They don’t like spending money on repairs or renovations.

“I live in Perth. Our experiences are wildly different from those of Sydney or Melbourne, especially for houses. I’ve seen many people selling properties at a loss – after anything up to 15 years. And this has happened while eastern state capitals have seen massive price growth.”