For many of us, buying a home remains one of the most stressful and frustrating experiences we will ever undertake.

Despite advances in digital banking, identity verification and broader financial innovation, the UK homebuying process continues to rely on fragmented systems, repeated checks and duplicated paperwork. The result is a transaction process that is slow and, because of that, more likely to fail.

The statistics bring the scale of that challenge to life.

The average UK property transaction takes around 22 weeks to complete, nearly one in three transactions collapses before completion and approximately 530,000 sales fall through each year. This costs consumers an estimated £560 million in wasted fees and creates wider economic losses approaching £1 billion annually.

Perhaps most strikingly, research undertaken through the first phase of CFIT’s Open Property Coalition found that less than 1% of the information required to buy a home is fully digitised.

DISCONNECTED PROCESSES

The mortgage market has, of course, invested heavily in digitisation over recent years, but the wider property ecosystem still operates through disconnected processes and information silos.

Buyers, lenders, brokers, conveyancers, estate agents and surveyors frequently request, verify and exchange the same information multiple times throughout a transaction.

As we all know, this sadly creates avoidable delays, operational inefficiencies and uncertainty for everyone involved.

That is why I believe Smart Data principles can play a transformative role.

MODERNISE HOMEBUYING

CFIT’s recently published Open Property Roadmap – developed through the UK’s first Smart Data coalition of its kind beyond financial services – sets out how secure, consent-driven and interoperable data sharing could modernise the homebuying process in much the same way Open Banking transformed financial services.

The core principle is straightforward: verified information should be reusable across the transaction lifecycle rather than recreated at every stage.

Today, a buyer may provide identity information, source-of-funds evidence and financial documentation multiple times to different organisations. Each participant then undertakes its own verification processes, creating duplication and delay.

In a Smart Data enabled process, trusted information could move securely between authorised participants with the consumer’s consent, reducing those frictions I describe whilst maintaining appropriate safeguards and auditability.

DIGITAL PROPERTY ID

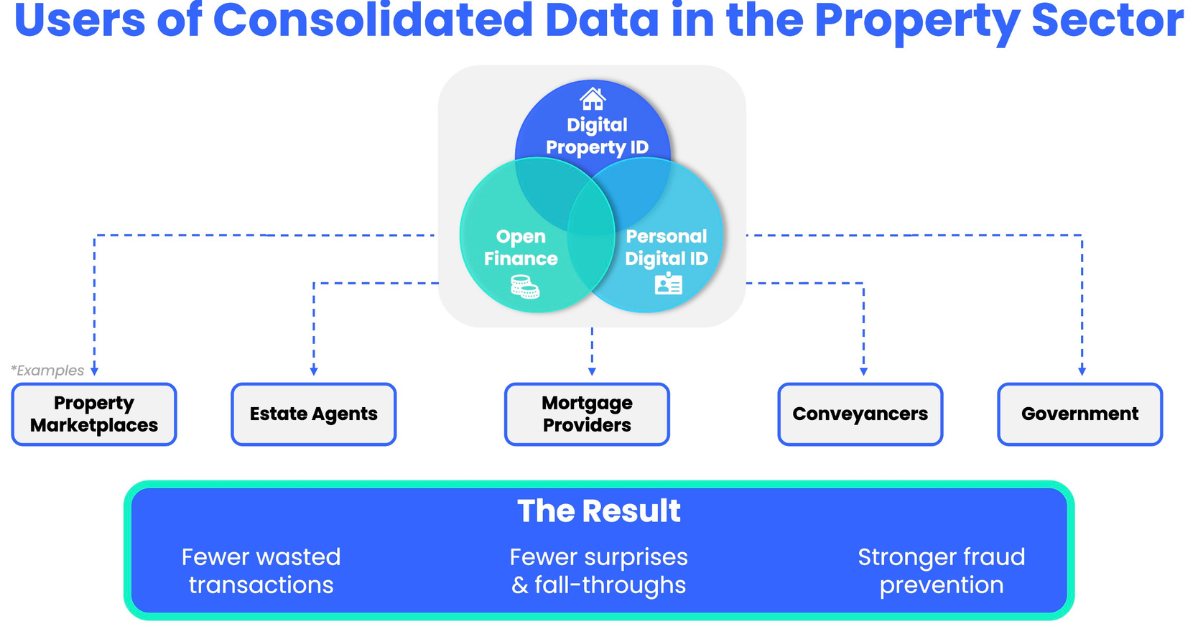

At the centre of our Roadmap is the concept of a Digital Property ID – a reusable framework of verified property information linked to a Unique Property Reference Number (UPRN).

This could bring together information such as title and ownership data, Energy Performance Certificates, planning history, transaction milestones and mortgage-readiness indicators into a structured and reusable framework.

However, the opportunity here could extend beyond property information alone.

A successful home purchase depends on three key categories of data: property data, identity data and financial data. Together, these form the foundations of underwriting, affordability assessments, source-of-funds checks, compliance processes and transaction progression.

The opportunity here is therefore not simply a Digital Property ID, but what might be thought of as a “Smart Data Pack” – a trusted combination of verified property, identity and financial information that can move securely across the transaction chain.

For lenders and brokers, the implications could be particularly significant.

Earlier access to verified source-of-funds information could accelerate decision-making.

Trusted digital identity credentials could reduce onboarding friction.

Better visibility of transaction milestones could improve pipeline management and customer communications.

And enhanced interoperability could reduce manual processing and rework across multiple parties.

FASTER UNDERWRITING

The Open Property Roadmap identified opportunities including earlier source-of-funds verification, improved fraud detection, shared transaction tracking and faster mortgage underwriting as some of the highest-value use cases for early implementation.

Importantly, this is not about creating a new central database or replacing existing market participants.

Much of the underlying infrastructure already exists. Open Banking rails, digital identity solutions, property datasets and emerging interoperability standards are already available.

What has historically been missing is coordination across the ecosystem, alongside clear frameworks governing trust, consent, liability and data sharing.

“That is why collaboration going forward is so important.”

That is why collaboration going forward is so important. Our Open Property Coalition brings together lenders, brokers, property firms, technology providers, regulators and government to develop practical solutions for implementation.

Rather than focusing solely on technology, the Coalition examines the governance, trust and interoperability frameworks required to enable trusted data reuse at scale.

The next phase of the programme will now focus on turning those recommendations into reality.

The level of support behind this agenda was evident at the recent Open Property Roadmap Showcase, which brought together senior representatives from across government, lenders, brokers, conveyancers, technology providers and the wider property ecosystem.

The event marked the culmination of the Coalition’s first phase and demonstrated a growing consensus around both the scale of the challenge and the opportunity presented by Smart Data.

More importantly, it highlighted a strong appetite across the market to move beyond diagnosis and into practical delivery.

That momentum now provides a strong foundation for the next phase of the programme as industry works together to test, refine and implement the solutions set out in the Roadmap.

Phase 2 of the Coalition will proceed in the summer with the discovery phase, prototyping and implementation. Workstreams will focus on product development, trust and interoperability frameworks, and commercial sustainability models designed to support long-term adoption.

Participating lenders and mortgage firms will play a central role in shaping and testing these solutions.

BIG OPPORTUNITY

The UK has already demonstrated global leadership in financial innovation through initiatives such as Open Banking. Open Property represents an opportunity to apply those same Smart Data principles to one of the UK’s most important markets.

Modernising the homebuying process is no longer simply a technology ambition. It is increasingly an economic necessity.

The opportunity now is to build a more connected, transparent and efficient property ecosystem that works better for consumers, lenders, brokers and the wider economy alike.