Sherlok’s system is used to manage $70 billion in mortgages, including by brokers at one of the largest aggregators, AFG. Of the 36,500 loans negotiated in the six months to December 2023, the highest discount on an existing rate for a broker using the system was 2.8 per cent, while one customer received $35,400 in annual savings by repricing.

The Mortgage & Financing Association of Australia said in a report last week that 88 per cent of brokers had negotiated a better rate with a borrower’s current lender. It comes as APRA still requires lenders to add a 3 per cent buffer when assessing new loans, meaning borrowers seeking to switch are being assessed at their ability to repay at a mortgage rate of around 10 per cent.

“Borrowers have become unable to refinance with a new lender because they cannot meet the serviceability criteria that lenders use to assess loan applications, but many existing borrowers have been able to re-negotiate with their current lender, or refinance with a new lender on more favourable terms,” MFAA CEO Anja Pannek said.

Refinancing comeback

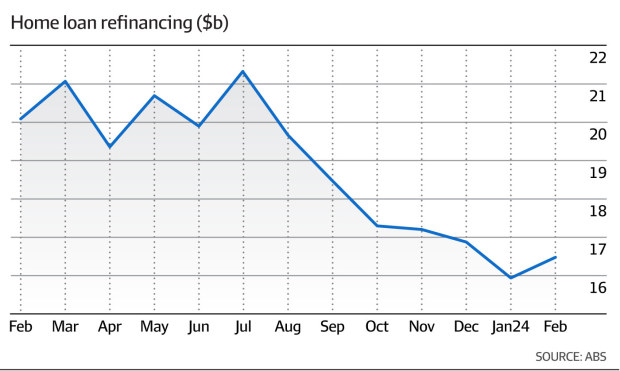

The number of home loans being refinanced each month staged a small comeback in February, with ABS Lending Indicator data last week showing $16.55 billion of refinancing in February, up $478 million. But that followed six consecutive months of declines. The current value of externally refinanced loans is almost a quarter lower than its peak last July, when $21.53 billion of mortgages were refinanced.

Banks’ focus on discounting for existing customers presents an additional headwind for lending margins. Three of the major banks – National Australia Bank, ANZ Bank and Westpac – will report half-year results during the first week of May, when analysts expect margins will continue to be squeezed amid soft growth for credit more broadly.

“We forecast average major bank loan growth of just 1 per cent half on half in the first half, with 2 per cent growth in Australian mortgages,” Morgan Stanley analyst Richard Wiles said in a preview of the upcoming results last week. “We think that growth will remain modest this year even if there is a rate cut, and management commentary won’t be bullish on the outlook.”

Morningstar senior equity analyst Nathan Zaia said in a report on Friday that credit growth has eased as higher interest rates and inflation have reduced borrower capacity. Total growth slowed to an annualised 4 per cent.

“Net interest margins are softening with competition in loan and customer deposit rates,” Mr Zaia said. “When banks had a large loan book on higher rates, cheaper loans to new customers could be made with the bank still achieving strong returns overall.”

The latest set of lending data from the prudential regulator for February showed ANZ had the most momentum in owner-occupier mortgages; it grew by 0.4 per cent month-on-month. Commonwealth Bank and Westpac grew at the sector average of 0.3 per cent month, while National Australia Bank was more selective, at 0.2 per cent month-on-month growth. Bendigo and Adelaide Bank, Bank of Queensland and Macquarie all grew at faster rates in February than the majors.

Too long to switch

The MFAA renewed calls last week for banks to streamline the process of discharging existing loans for customers wanting to switch, describing this as “an unsatisfying experience and the pain points continue to impede the process of switching lenders”.

Five years after the Australian Competition and Consumer Commission said it should take 10 days for a mortgage holder to switch banks, data from digital broker Lendi, reported by The Australian Financial Review last month, showed most customers are waiting double that time. The issue was raised by ACCC chairman Gina Cass-Gottlieb at The Australian Financial Review Banking Summit last month.

“Discharge timeframes continue to be lengthy, causing customers to miss settlements, pay more in fees and interest and experience a lengthy and complex process overall lenders are increasingly using retention tactics to try and save the customer from discharging their mortgage,” the MFAA said.