(ARR)")

PM Images

From 2020 through last year, I had a bearish outlook on most mortgage REITs, specifically those with significantly leveraged exposure to long-term residential mortgage-backed securities. Going back to my bearish outlook on ARMOUR (NYSE:ARR) from September 2020, I expected mortgage rates to rise as the Federal Reserve slowed and reversed its immense quantitative easing effort into the residential mortgage-backed security “RMBS” market. Since ARMOUR has leveraged exposure to the RMBS market, I expected a sharp decline in its book value stemming from declines in RMBS values relative to Treasuries.

That is essentially what has occurred. Mortgage rates spiked once the Federal Reserve stopped buying them in 2022, leading to catastrophic book value declines for ARMOUR (as well as many regional banks). See below:

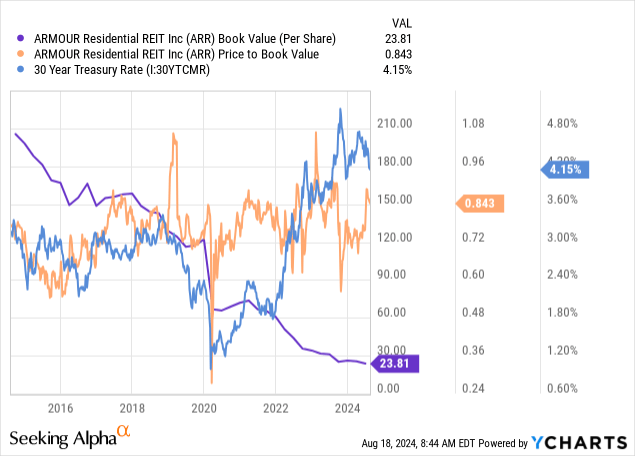

Mortgage REITs often trade near their book value. Since ARR’s book value usually declines, it tends to trade at a price-to-book ratio of ~65% to ~90%. It is currently at a “P/B” of 84%, indicating it is at the upper end of its normal valuation range, potentially pointing toward improving sentiment.

I last covered ARR in October 2023, expecting a 50% dividend cut by 2024 as its interest rate swaps expired. Instead, its dividend was cut by 40%, in-line with my estimate. Since then, ARR has lost an additional 5% of its price, though it had fallen by over 36% as dividend concerns grew, rebounding. Its overall returns are decent, with an 11.9% return if dividends are included.

Short interest on ARR is not excessive but notable at ~9%, indicating a fair amount of negative sentiment remains. That said, I believe the worst is likely over for ARMOUR. Ironically, negative economic headwinds may be a boon for ARMOUR, as they may discourage further QT to RMBS assets and could result in bond market stimulus that could substantially improve ARMOUR’s book value. Historically, lower rates have not benefited ARR dramatically because that often increases refinancing risks. However, given the bulk of its balance sheet is at lower rates, I believe this risk is lower than in the past.

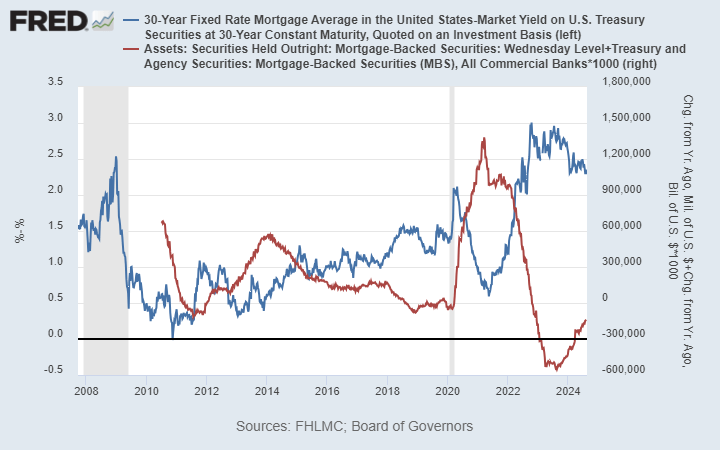

Mortgage Spreads Appear to be Falling

ARMOUR’s business model is straightforward. It borrows money in short-term markets to buy long-term residential mortgage-backed securities. Most of its assets have near 30-year maturities, are fixed, and are guaranteed by agencies like Fannie Mae (OTCQB:FNMA) and Freddie Mac (OTCQB:FMCC). Those agencies should significantly limit their credit exposure, though the US government has no obligation to bail them out again if need be.

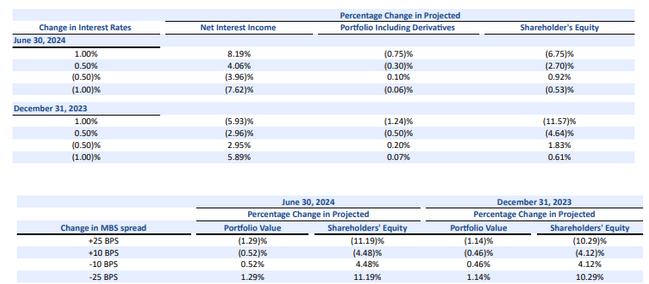

ARMOUR hedges its direct exposure to long-term interest rates through Treasury market derivatives. However, like most, it cannot hedge against the risk of mortgage rates rising faster than Treasuries, otherwise known as the “MBS spread.” This critical component fueled my bearish outlook for ARMOUR, as the MBS spread is also correlated to the Federal Reserve’s heavy hand in the mortgage market. See its equity sensitivity to interest rates:

ARMOUR REIT Interest Rate Sensitivity (ARR 10-Q Q2 2024)

The bulk of its exposure to interest rates is mitigated through hedging. A 1% interest rate cut is expected to lower its book value by a mere 53 bps, while a 1% rise would lower its book value by an expected 6.75%. The impact on its net interest income would be larger, with rate declines reducing its expected income by 7.6%. Importantly, its hedging is from 30-year-long Treasury rate futures and rate swaps of varying maturities (~5-year weighted-average term at ~1.9%).

So, this exposure is not from a change in the short-term rate by the Federal Reserve but across the yield curve, with more focus on the long end. Upcoming rate cuts will not change its book value unless they also result in changes to long-term Treasury rates and, more specifically, the spread between them as long-term mortgage rates. Federal Reserve rate cuts will lower its direct borrowing costs; however, they should have a limited impact on its overall net income due to its interest rate swaps.

Still, the key metric to watch is the spread between long-term mortgage and long-term Treasury rates. As indicated in the latter section of the table above, a 25 bps decline in that spread should improve ARMOUR’s book value by ~10.3% and vice versa.

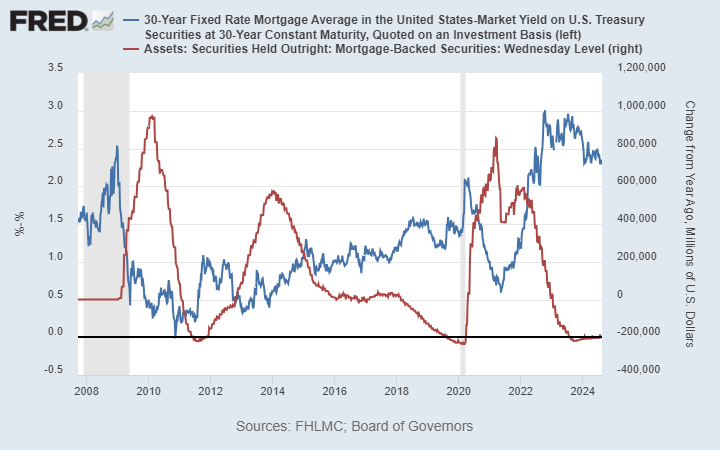

The mortgage spread is high today, with borrowing rates being, on average, 2-2.5% above the 30-year Treasury rate. Usually, that spread is closer to 1%. However, it has varied dramatically with the Federal Reserve’s purchasing or selling (through maturation) trend of MBS assets. See below:

Annual change in Fed Reserve MBS assets vs. MBS spread to Treasuries (Federal Reserve Economic Database)

Generally, MBS spreads usually decline when the Federal Reserve expands its MBS holdings. That was seen from 2009 to 2011, briefly around 2013, and from 2020 to 2021. Conversely, periods of near-zero or negative Fed ownership trends, such as 2016-2019 and since 2022, are usually associated with higher MBS spreads.

Although the dataset is smaller, we can see an even more apparent pattern by accounting for changes in commercial bank MBS assets. Banks often follow the Federal Reserve’s buying and selling trend, but not always. Today, banks are again buying MBS assets after selling them in 2022, going against the Federal Reserve. The combined annual change is still negative, but the monthly change of the combined figure is flat.

Fed Reserve plus commercial bank MBS purchases vs. MBS spreads (Federal Reserve Economic Database)

The post-2008 financial market is liquidity-driven. When a small number of participants, such as the Federal Reserve and a few large banks, buy and sell hundreds of billions in securities, they will considerably impact prices. I believe mortgage rates were meager in 2021 due to excessive liquidity pouring into the MBS market from both the Federal Reserve and commercial banks. The opposite was confirmed in 2022 and early 2023, as the Fed’s QT program and inflation caused immense devastation from higher mortgage rates (and spreads).

Today, the market is calm. The Fed’s MBS balance sheet continues to unwind, but banks are buying in again. Indeed, they (30-year mortgages at ~6%) appear attractive due to their high premium to Treasuries of equal maturity and the odds that disinflation will cause long-term bond yields to decline.

This could be excellent news for ARMOUR. If MBS spreads decline back to 1% from the current ~2.5%, it will gain from a ~150 bps spread decline. A 25 bps spread decline is associated with a 10.3% expected book value gain. We can’t assume this relationship is entirely linear, but a 150 bps drop could result in a 40-50% book value gain, depending on the fine details of its hedging profile.

Since I believe mortgage spreads will decline, though not necessarily back to their historical median, I have a bullish outlook for ARR. The best outcome for ARR would be ending the Federal Reserve MBS balance sheet sakes. Thus far, the Fed has slowed the pace of its MBS sales to ease associated mortgage rate concerns, a critical positive step in that direction. Should the economy enter a recession, I expect the Fed to quickly bring QE back to the MBS market due to the high political value of keeping mortgage rates in check.

ARMOUR Still Faces Critical Risks

There are two key risks facing ARMOUR. One, in the event of a slowdown, MBS spreads could rise, not fall, due to perceptions of risk surrounding the financial stability status of Fannie Mae and Freddie Mac. Even if those two firms are likely to meet obligations in a recession, if investors fear they will not, MBS assets could temporarily lose enough value that ARMOUR faces a margin call. This can also occur due to a decline in market liquidity. ARMOUR faced that issue during the April 2020 crash, forcing it to realize significant losses.

I have debated this issue as economic trends, and my understanding of them has evolved. However, I currently believe that, under normal circumstances, it is highly unlikely that we will see an increase in mortgage delinquencies like that of 2008. As I recently discussed regarding Fannie Mae, the company is better capitalized than it used to be. Still, it does not have enough equity to meet a massive increase in mortgage defaults.

However, although home affordability is extremely low, most US homeowners are paying far less on their mortgage debt service than they used to. Today’s mortgage debt service-to-disposable income ratio is around two-thirds its 1990s level and around 45% lower than it was at the 2006 peak.

Indeed, since 2022, a cohort of new home buyers has been paying abnormally high mortgage rates at oddly high home prices. Thus, I think there is a high default risk in MBS with >6% yields, as those are likely associated with potentially overextended borrowers.

Still, across the US economy, most homeowners bought at low prices after 2008 and refinanced to ultra-low mortgage rates before 2022. Outside of a severe economic crisis, I believe the default risk of most homeowners is extremely low.

Even more because most homeowners are paying a low rate, the odds of them refinancing should rates fall are low. Historically, ARMOUR has seen book value declines irrespective of mortgage rates because they were falling to such extreme lows that refinancings rose or mortgage rates spiked, devaluing low-rate mortgages.

Looking at ARMOUR’s investment summary (10-Q pg. 38), we can see the bulk of its MBS assets are at a ~5% yield. This implies it sold many of its older MBS assets and purchased more minted since 2022. So, should mortgage rates decline below 5%, around half of its assets could have refinancing risk. However, only around $600M of its securities ($9.2B total) have a 6.5% yield. Realistically, most homeowners would only refinance if they can get at least a 1% rate reduction, so I expect refinancing levels to be very low outside of an unlikely return to sub-3% mortgage rates.

Further, although these “young” mortgages are likely at higher default risk because they may be toward overextended borrowers, they represent a small portion of the overall MBS market. As such, I expect that Fannie and Freddie can meet their obligations to guarantee defaults, limiting ARR’s credit risk in a recession. Still, it may be wise to monitor that risk, as a very “hard landing” may create sufficient concern in this issue.

The Bottom Line

I am now speculatively bullish on ARR, expecting its book value to increase as MBS spreads decline. A soft landing that normalizes inflation and rates would be ideal for ARMOUR. However, I expect it may do well in a recessionary environment, mainly if the Federal Reserve eases mortgages. I believe the Fed’s potential reluctance to spike inflation again through QE will be offset by political pressure to ease mortgage concerns. That is the historical precedent from 2008 onwards.

Unlike in the past, ARMOUR’s refinancing risk from lower rates appears low, meaning its book value may finally end its devaluation trajectory. I would not be surprised to see ARR crash if stocks do, since it is highly exposed to liquidity in the MBS market. That said, I believe moderate-to-severe disinflation, potentially combined with Fed easing, would be very bullish for ARR.