St. James’s Place’s investment team shares its view on global markets, examining geopolitical tensions, economic uncertainty, and central bank policies, while highlighting opportunities in international equities, UK stocks, and bonds.

Justin Onuekwusi, Chief Investment Officer at St. James’s Place, comments: “As we enter the final quarter of the year, global markets remain shaped by persistent macroeconomic uncertainty, diverging central bank policies, and ongoing geopolitical tensions. However, in an historic move, Israel and Gaza have this week signed the first phase of a peace deal. This opens the way for a ceasefire and has strengthened hopes of an end to the war. Meanwhile this month saw a government shutdown in the US as the Republicans and Democrats failed to reach an agreement on spending plans.

“Despite this challenging backdrop, markets, particularly in the US and Europe, have shown resilience, underlining the importance of staying the course – being both grounded in fundamentals and flexible to change. We are closely monitoring geopolitical and market developments and adjusting our approach accordingly. Here’s an overview of how we view the market and what it means for SJP’s portfolios.

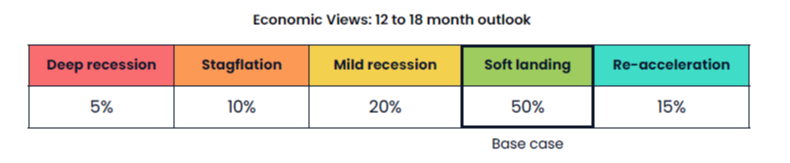

Hetal Mehta, Chief Economist at St. James’s Place, said: “We estimate that the risks of a deep recession have moderated slightly, given recent economic data and developments. There is not yet sufficient confidence to formally lower our recession probability, which remains at 35%. But a soft-landing scenario (in which the economy slows but avoids recession) remains our base case.

“There is little sign of an end to the volatility seen so far this year. Geopolitical turbulence has seen Russia step up its attacks on Ukraine. It is also believed to be behind drone incursions in Europe, notably in Denmark, Estonia and Poland. These ‘tests’ of Europe’s resilience are fuelling uncertainty for investors. The conflict in the Middle East intensified but more recently there have been signs that a peace deal could potentially be reached.

“Trade tensions appear somewhat less disruptive than in the previous quarter. President Trump’s recent state visit to the UK saw the signing of a multi-billion-dollar trade agreement between the two countries. The so-called ‘Tech Prosperity Deal’ could see firms such as Google and Microsoft investing billions in the UK. However, a new raft of tariff announcements, including on the pharmaceuticals and film industries could temper optimism.

“The recent US government shutdown over spending plans is something the team will be watching carefully. However, if it ends up being a short shutdown only, it is unlikely to have notable economic impact. To date, investors have shown no sign of being spooked, with stocks rising globally.

Justin Onuekwusi, Chief Investment Officer at St. James’s Place, comments: “We continue to review the house view and asset allocation and have made no changes this quarter as current allocations continue to reflect our medium-term views. While global markets do appear expensive compared to history, this is largely driven by the US. Other regions look more reasonably valued and have been benefiting from positive momentum this year.

“We remain underweight the US and overweight developed markets (DM) excluding US, given the stretched valuations, heavy market concentration and difficulty repeating past returns. They also have a positive view on EM which are attractively priced relative to DM, with significant variation between regions within EM. Global small caps and particularly those in Japan are compelling from a valuation and earnings perspective.

“Bond markets still offer good income, especially corporate bonds, where fundamentals remain solid. Government bonds also look reasonably valued but concerns about inflation and rising debt are making investors more cautious.

“In the UK, the economy appears more balanced than in the last quarter, with an improvement in market performance. This has been supported by expectations of rate cuts and, increasingly, corporate adoption of AI. UK equities remain one of the most undervalued globally — second only to China — and continue to offer attractive shareholder yields. We see selective opportunities in UK small-cap, growth, and value stocks.

“However, fiscal constraints remain a challenge and the upcoming November Budget looks unlikely to close the budget gap. Labour’s manifesto commitments are likely to limit the Chancellor’s room to respond to any economic downturn. It is worth noting however that while the UK economy may remain under pressure, many UK companies generate much of their revenue from international markets.

“In the US, equities have rebounded strongly from weakness earlier in the year and remain near all-time highs. Profitability remains a key driver of performance, with large-cap growth stocks continuing to lead. However, while the dominance of the seven largest tech companies was causing concern, there are now signs of broader earnings recovery beyond the mega-cap complex. US equity valuations remain high, however, trading at a significant premium to their global peers.

“Market performance across continental Europe has also improved, with increased business optimism and a strengthening euro. Resolution on trade tariffs and strong exports has also helped. However, there are still challenges ahead and our optimism is cautious.

“Emerging market equities have delivered some of the best performance year-to-date, with China showing signs of cyclical improvement from a very low base.

“The team continues to be positive on small caps, which have shown renewed strength, particularly outside the US. International small caps — led by Japan and Europe ex-UK — have notably outperformed US small caps so far this year. Compelling factors include historically low valuations and a supportive macro backdrop. Yet while US small caps face near-term profitability challenges, they retain attractive long-term growth potential.

“International small caps currently offer a return on earnings above historical averages and stronger earnings growth outlooks than their large-cap counterparts. Given this, we believe there is a real opportunity for strong returns in the coming years.

“Within fixed income, sovereign bond yields remain attractive in nominal terms, suggesting fair value. However, sticky inflation and rising fiscal risks (especially in the US and UK) are ongoing concerns. Overall, the balance of risk and reward remains finely poised.

Key takeaways

“While we are underweight US compared to the broader market, we have good exposure, and it remains our largest equity position. We are striking a deliberate balance – cautious on valuations, but mindful of the long-term importance of the US in global portfolios.”